Sydney J. Harris rightly said, “Happiness is a direction, not a place” and today all economies in the world are struggling to walk in this direction. A step to achieve this was taken in the UN Sustainable Development Solutions Network in 2012 when they adopted resolution 65/309: Happiness: Towards a Holistic Definition of Development. This was done to invite the 149 member countries to measure the level of happiness among their population and use these numbers to guide public policy. Although the World Happiness Reports have been based on a wide variety of data, the most important source has always been the Gallup World Poll, which is unique in the range and comparability of its global series of annual surveys.

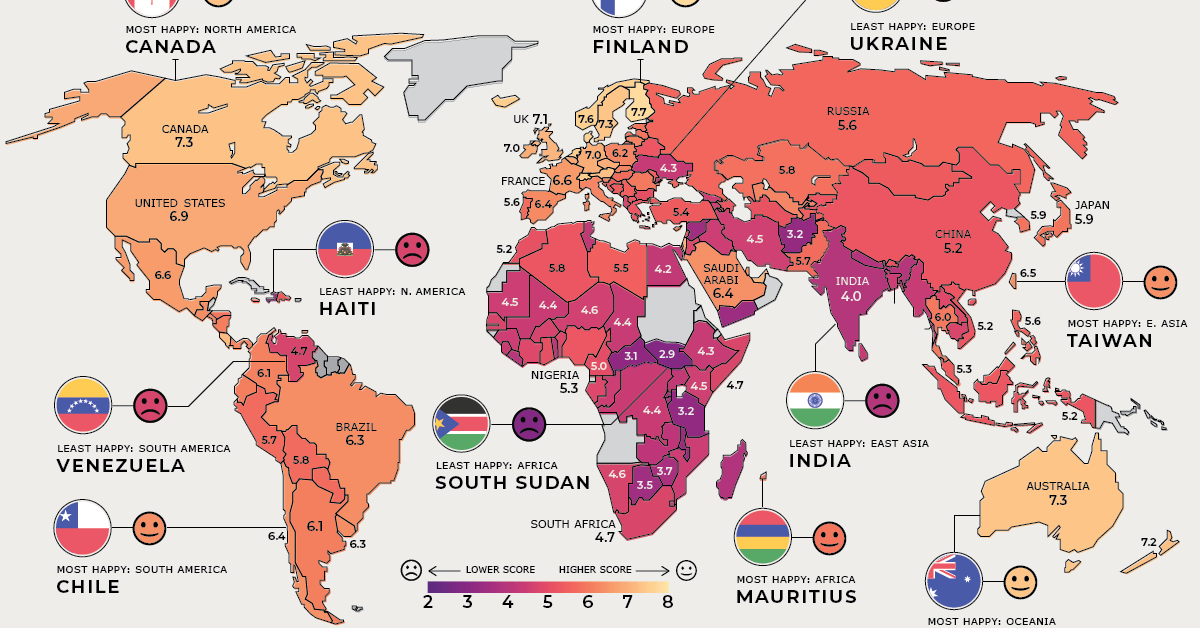

Finland has been ranked number 1, being the happiest country in the world for the past few years. India has always been very low on the happiness index, averaging around 125th. In fact, in 2021, India was ranked 139 out of 149 countries. The results of the happiness index are correlated with a lot of factors including GDP, social security, personal freedom, life expectancy and opinions of residents among others.

As former President, Dr Pranab Mukherjee commented, “Despite our country’s economic progress, India is constantly going downwards in the happiness index. This indicates a lack of a holistic approach towards development.” According to him, the best step that the policymakers of the country should take is to adopt the ‘triple bottom line’ accounting framework. It focuses on all essential aspects of holistic development of individuals including social, ecological and financial development. This also implies that happiness is weakly correlated with wealth and the economic growth of a country.

According to the economist and author Jayshree Sengupta, India has been ranked poorly on the happiness index due to various reasons. Some of these are rapid urbanization and congestion in cities, concerns about food security and water safety, rising costs of healthcare, women’s safety, and environmental pollution, which itself is linked to poor mental wellbeing. These conditions have worsened over time and were amplified due to the Covid-19 crisis.

The ever-growing inequality between the rich and poor of the country is another crucial reason for the chronic unhappiness. During the Covid crisis, India reportedly added 40 new billionaires to the global list while about 57% of the working class in the country were on the verge of losing their jobs. This growing pay gap in the population has worsened the mental wellbeing and hence the happiness of the population.

A statistical exercise using variables like GDP per capita, social support, healthy life expectancy, freedom to make life choices, generosity, perceptions of corruption and dystopia was done to understand the relationship of these indices with the happiness index. It found that all these variables are statistically significant and thus have significant explanatory power. They illustrate that on average richer countries fare better on subjective evaluations of life circumstances, as do nations with more social support, lower levels of corruption etc.

Why India, despite its high level of economic growth ranks so low is because it ranks very low on some of these indices. For social support, India is ranked 142nd out of 149 countries. However, if we consider Pakistan’s ranking on all of these individual indicators, it is very similar to India and worse in some cases. According to this, India should be ranked one spot above Pakistan but that is not the case. Pakistan is ranked 105 while India is ranked at 139. This points out to predictive anomalies that this model has.

One reasonable explanation for this could be that people in India have higher expectations and thus also have greater disappointment. This is one of the very crucial reasons for the low happiness ranking in India in addition to the increasing income inequality and feelings of injustice and unfairness because of the structure of the society and its history. Thus, better political leadership and public policy framework in India are essential for improving the happiness index of people in India.

Picture Credits: Visual Capitalist

Aanya Poddar is a third year undergraduate student at Ashoka University. She is pursuing a BSc. (Honors) in Economics and Finance. She is the President of the Ashoka Economics Society.

We publish all articles under a Creative Commons Attribution-Noderivatives license. This means any news organisation, blog, website, newspaper or newsletter can republish our pieces for free, provided they attribute the original source (OpenAxis).

{kind=link}